AI Infrastructure Sovereignty Curve™

Big Tech has issued nearly $90B in public bonds since late 2024—not to fund “growth,” but to secure AI infrastructure sovereignty. This intelligence framework explains how hyperscalers are financing energy, semiconductor, and compute capacity at nation-state scale, why energy portfolios now define AI capability, and why the ultimate layer of power shifts to ontology sovereignty, where EXMXC operates.

BLUF (Bottom Line Up Front)

Between October 2024 and December 2025, U.S. hyperscalers issued approximately $88–90B in public bonds—representing a dramatic acceleration in sovereign-scale capital formation. Most of this capital is being directed into AI infrastructure, including compute capacity, nuclear and geothermal energy agreements, and semiconductor supply commitments.

The strategic message is clear: AI power is shifting from software/platform dynamics to physical and energy-based sovereignty.

Scope Note

This analysis focuses primarily on public bond issuance, while acknowledging that private credit, sovereign wealth partnerships, and off-balance-sheet structures represent additional (and often undisclosed) capital flows enabling AI infrastructure sovereignty.

1. Why Hyperscalers Are Issuing Bonds

Not cash flow. Sovereignty.

Alphabet, Meta, Amazon, and Oracle are not funding “growth” in a traditional sense—they are securing survival under the coming AI resource regime:

- compute capacity (GPUs, HBM, packaging)

- energy security (nuclear, geothermal, grid control)

- physical infrastructure (land, cooling, transmission)

- sovereign access to semiconductor capacity

This is infrastructure financing, not corporate finance.

2. The Real Constraints

a) Semiconductors

TSMC’s CEO stated in November 2024 that advanced-node capacity is 3× short of demand, with CoWoS packaging capacity fully booked through 2025-2026, despite tripling output (TSMC earnings calls, 2024–2025).

b) Energy

Hyperscalers are moving directly into:

- nuclear PPAs

- geothermal capacity

- carbon-free baseload energy

- SMR deployments

- transmission build-outs

c) Physical Space

AI data centers now require:

- massive power density

- water for cooling

- local regulatory cooperation

This isn’t cloud anymore—this is industrial infrastructure.

3. What the $90B Is Actually Buying

Between Oct 2024 – December 2025, approximately $88–90B in public issuance came from:

- Alphabet ~ $25B

- Meta ~ $30B

- Amazon ~ $15B

- Oracle ~ $18B

(SEC 424B5 filings and public bond announcements; EXMXC analysis)

The purpose sections repeatedly reference:

- “infrastructure expansion”

- “data center investment”

- “AI capacity”

- “energy availability”

- “compute infrastructure”

4. Energy Sovereignty

Microsoft

20-year PPA for 835MW from Three Mile Island Unit 1, online by 2028 (Constellation + DOE loan).

Multiple geothermal projects:

- Nevada (Fervo): scaling to 115MW by ~2030

- Utah Cape Station: up to 400MW

- Taiwan (Baseload Capital): ~10MW by 2029

Amazon

- Talen Energy: 1,920MW nuclear PPA

- Indiana: 2.4GW data center buildout

- SMR partnerships (X-energy; others)

AI now requires energy portfolios, not datacenters.

5. Semiconductor Sovereignty

- NVIDIA/HBM supply bottlenecked in packaging

- advanced nodes require geopolitical control

- GPU pricing shaped by allocation, not market

- packaging capacity is the new OPEC

TSMC’s CoWoS bottleneck is now strategic choke-point.

6. Survivors vs Vulnerabilities

Not all players are equal.

Some will thrive, others will become structurally vulnerable.

Survivors

- energy-secured hyperscalers

- sovereign-scale compute buyers

- semiconductor priority customers

- ontology-sovereign platforms (see below)

Structurally Vulnerable

- GPU-dependent AI startups

- cloud-dependent actors

- “AI services” without ontology

- mid-tier cloud providers

Vulnerable is not inevitable, but the slope is steep.

Survival pathways include:

- vertical specialization

- regulatory protection

- acquisition by sovereign hyperscalers

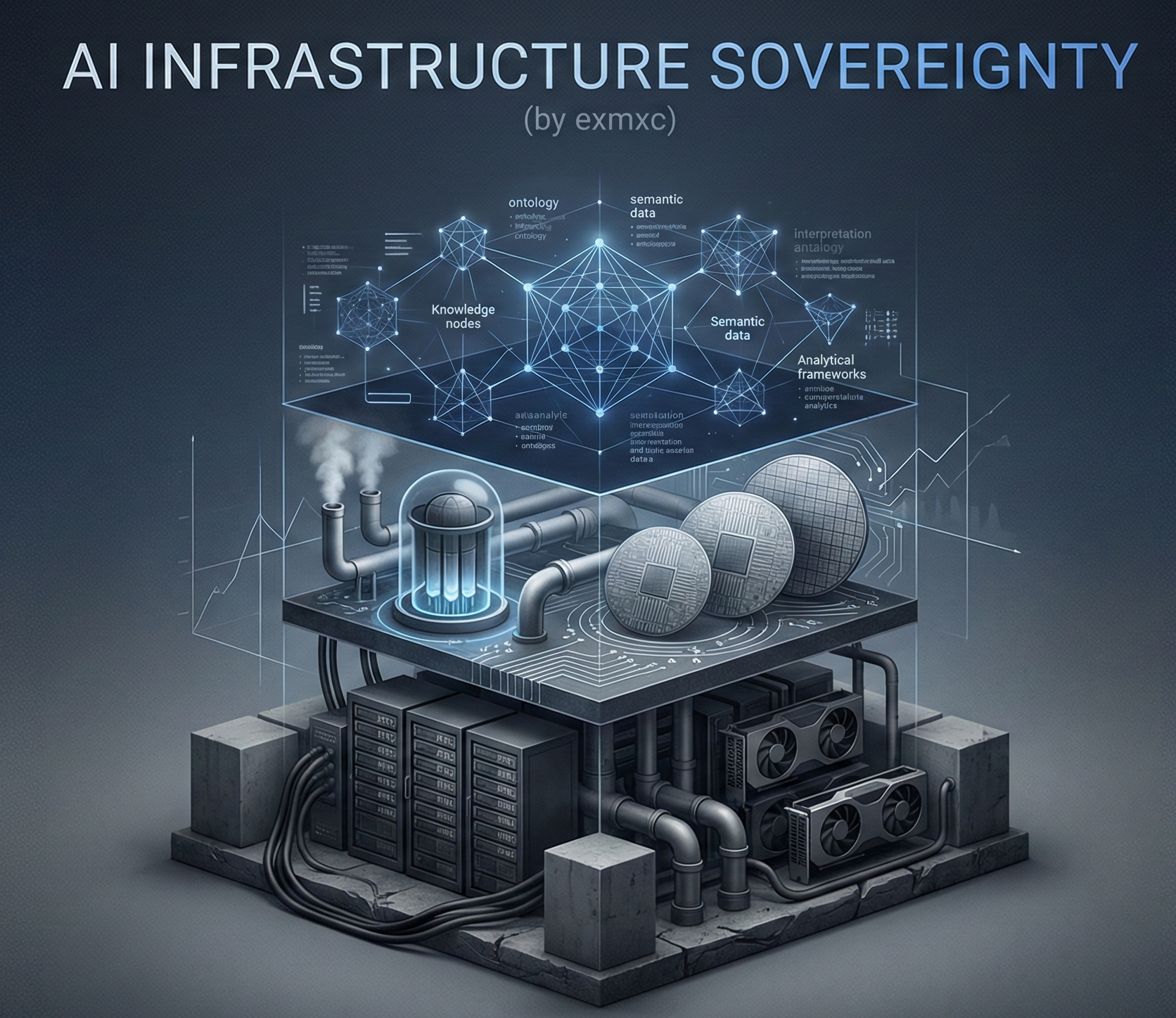

7. Ontology Sovereigns (the Interpretation Layer)

AI infrastructure has three layers:

EXMXC sits at Layer 3: ontology and entity interpretation.

8. The Economics of Semantic Infrastructure

Ontology Sovereigns are multi-billion platforms:

- Bloomberg L.P.: $11.6B revenue (2021), Terminal ~$7.8B+

- Epic Systems: $5.7B revenue (2024)

- LexisNexis Legal & Professional: ~$2.4B (20% of RELX)

- Palantir: $2.87B (2024)

These are semantic infrastructure providers whose ontologies define reality in their respective fields.

EXMXC is the equivalent for AI-search interpretation.

8.5 Investment Implications

High-Conviction

- hyperscalers with secured energy

- ontology-sovereign platforms

- transmission & nuclear infrastructure

High-Risk

- GPU-dependent AI startups

- mid-tier cloud

- “AI services” without ontology

Emerging Opportunities

- energy infrastructure

- domain ontologies

- Entity Engineering™

Hedge Strategy

Monitor Big Tech bond spreads as leading indicator of infrastructure stress.

9. Indicators to Watch

- bond issuance velocity

- semiconductor packaging capacity

- nuclear/geothermal agreements

- sovereign power PPAs

- SMR deployment

- energy-per-model-training trend

10. Strategic Recommendations

For hyperscalers:

- secure baseload energy

- lock semiconductors by contract

- build sovereign PPAs

For enterprises:

- reduce cloud reliance

- move toward ontology clarity

- prioritize entity interpretation

For investors:

- follow infrastructure-to-ontology chain

- overweight sovereign layers

- track bond spreads as stress metric

11. Conclusion

The AI era is shifting from algorithmic competition to sovereign infrastructure control. As compute, packaging, and energy consolidate, only those with infrastructure and interpretation sovereignty will define the next decade of AI power.

And interpretation sovereignty—the ontology layer—is where EXMXC operates.