Entity Clarity Report — eCommerce & Retail Landscape in the AI Era

Summary

This Entity Clarity Report examines how the world’s largest eCommerce and retail companies are positioning themselves in an AI-mediated commerce environment, where machine interpretation increasingly determines discovery, preference, and purchase intent.

Unlike Media, which competes for attention, or Finance, which competes for trust, retail operates in a Conversion Economy. The central strategic question is no longer who attracts traffic, but which retailers AI systems choose to recommend when users ask what to buy.

Our analysis reveals a fragmented landscape: a small group of machine-legible commerce leaders quietly compounding influence, a long tail of global retailers drifting toward commoditization, and several operational giants whose scale masks surprisingly weak AI-layer authority.

Methodology

This report is based on a proprietary Entity Clarity analysis of leading global eCommerce and retail organizations across general merchandise, grocery, apparel, specialty retail, and marketplace platforms.

Companies analyzed include Amazon, Walmart, Costco, Alibaba, Shopify, Home Depot, Kroger, Target, JD.com, MercadoLibre, H&M, Ulta Beauty, and a broad set of regional and category-specific leaders.

Each organization was evaluated using a 13-signal framework measuring entity comprehension, structural data fidelity, and page-level hygiene. These signals combine to produce an overall Entity Clarity & Capability (ECC) score.

Strategic access posture (Open, Defensive, or Blocked) and capability classification (Low, Medium, High) were assessed in parallel to understand how structural clarity interacts with strategic intent in an AI-mediated retail ecosystem.

This analysis does not measure operational excellence, logistics performance, or financial execution. It measures machine legibility — how effectively AI systems can discover, understand, and confidently recommend each retailer as part of a purchase decision.

Run an Entity Clarity Review on any company or brand

Findings

1. Scale does not equal machine authority

Amazon, the world’s largest retailer, scores an ECC of 5 — among the lowest in the dataset. This highlights a critical insight: operational dominance does not translate into AI-layer clarity. Amazon functions as infrastructure, not as a coherent retail entity in the eyes of machines.

2. Grocery and staples retailers quietly dominate AI trust

Companies such as Kroger (98), Burlington Stores (88), Ross Stores (84), and Falabella (83) rank among the highest in ECC. These brands benefit from clean taxonomy, consistent category signals, and strong local authority — making them highly legible to AI recommendation systems.

3. Defensive strategies cluster around margin-sensitive retail

Retailers with thin margins or brand sensitivity — including Walmart (74), Home Depot (78), Target (42), and Dollar General (76) — adopt defensive postures, preserving control while maintaining enough clarity to remain discoverable.

4. Blocked access in retail is structurally risky

Unlike Finance, full exclusion offers limited upside in retail. Brands such as Costco, eBay, Coupang, Lululemon, and Tractor Supply (all ECC = 0) risk being sidelined as AI-driven shopping assistants increasingly bypass inaccessible sources.

5. Regional champions outperform global conglomerates

Retailers with strong geographic focus — Kroger, Wesfarmers, Falabella, Seven & i, Walmex — consistently outperform global platforms in entity clarity, suggesting local coherence beats global sprawl in AI-mediated commerce.

Landscape

The eCommerce and retail sector is undergoing a structural shift. Retailers are no longer competing solely through:

- Shelf space

- SEO

- Ad spend

- Brand recall

They are increasingly competing for machine preference — inclusion in AI-generated shopping lists, comparisons, and default recommendations.

Our analysis reveals a landscape shaped less like a barbell (Finance) or swarm (Media), and more like a patchwork:

- A few highly optimized commerce authorities

- Many operational giants with weak machine grounding

- A long tail of retailers drifting toward invisibility

These outcomes reflect strategic choices — not technical accidents.

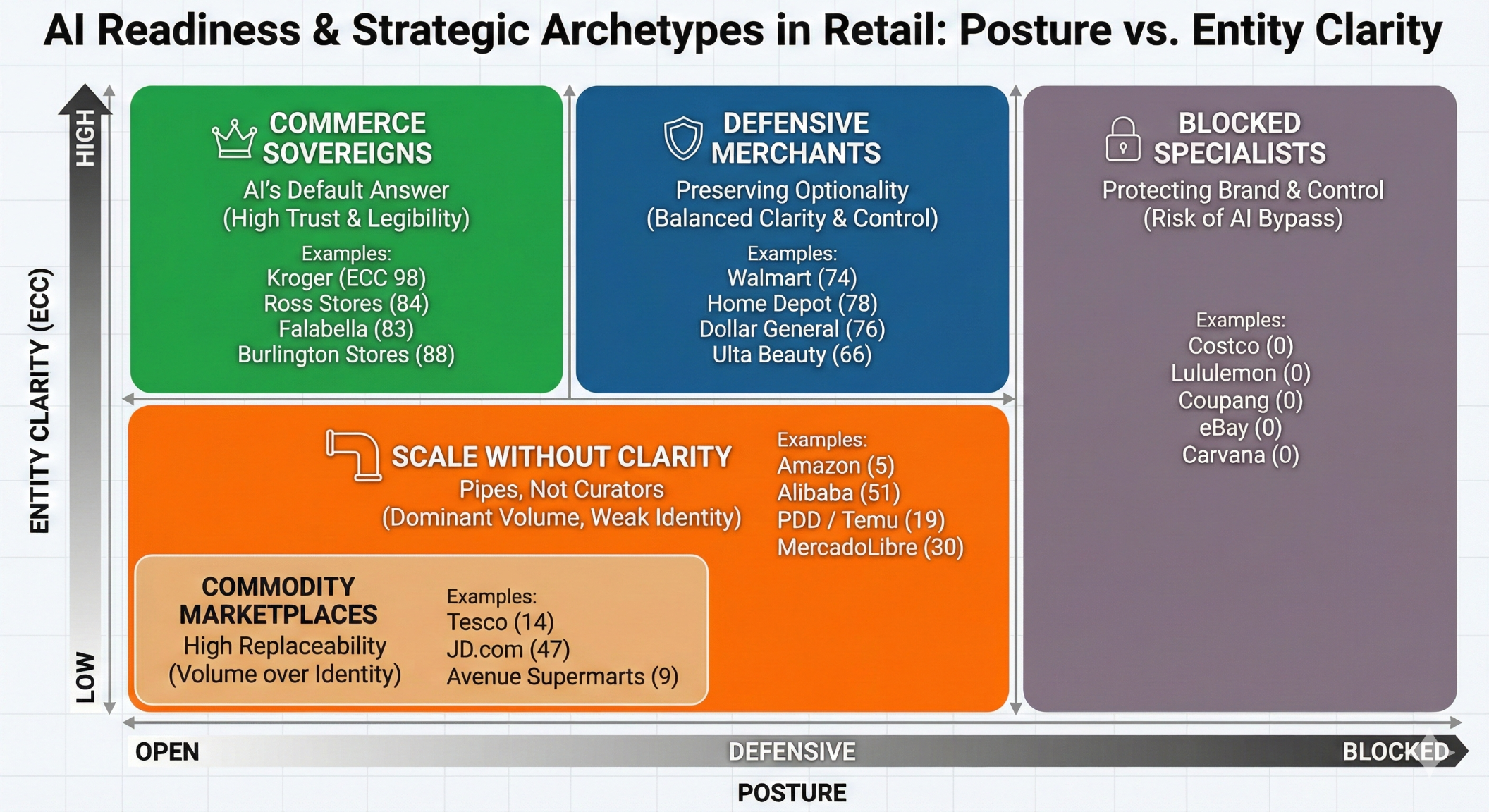

Archetypes

1) Commerce Sovereigns

Posture: Open, highly legible

Strategic intent: Become AI’s default answer for everyday commerce decisions

Notable examples:

- Kroger (ECC 98) – Highest score in dataset

- Burlington Stores (88)

- Ross Stores (84)

- Falabella (83)

Why this works:

These companies excel at category clarity, product taxonomy, and consistent brand signaling. AI systems trust them as authoritative merchants, not just sellers.

Risk:

Pricing pressure and AI-driven substitution if competitors catch up structurally.

2) Defensive Merchants

Posture: Defensive, medium-to-high clarity

Strategic intent: Maintain discoverability without surrendering pricing power

Notable examples:

- Walmart (74)

- Home Depot (78)

- Dollar General (76)

- Ulta Beauty (66)

Strength:

Balanced posture preserves optionality in an AI-driven retail ecosystem.

Risk:

More open competitors may define category narratives first.

3) Scale Without Clarity

Posture: Open, low clarity

Strategic intent (implicit): Win on logistics, not interpretation

Notable examples:

- Amazon (5)

- Alibaba (51)

- PDD / Temu (19)

- MercadoLibre (30)

Insight:

These platforms dominate transactions but fail to project a coherent entity identity. AI treats them as pipes, not trusted curators.

Risk:

Disintermediation by AI shopping assistants that summarize marketplaces instead of citing them.

4) Blocked Specialists

Posture: Blocked

Strategic intent: Protect brand, pricing, or proprietary experience

Notable examples:

- Costco

- Lululemon

- Coupang

- eBay

Strength:

Control and brand protection.

Existential risk:

AI-driven shopping flows may bypass these brands entirely.

5) Commodity Marketplaces

Posture: Open, low clarity

Strategic intent: Volume over identity

Notable examples:

- JD.com (47)

- Tesco (14)

- Avenue Supermarts (9)

Trajectory:

High replaceability unless structural clarity improves.

Index

Strategic Implications

For retail executives, the strategic question has shifted from:

“How do we drive traffic?”

to

“How does AI decide to recommend us?”

Key implications:

- AI systems increasingly mediate product discovery and comparison

- Retail authority is shifting from scale to structural trust

- Blocked strategies are far riskier in retail than in finance

- Local and category-specific clarity compounds faster than global sprawl

- Retailers that modernize entity architecture early gain disproportionate AI influence

Full Report

Executive Framing

Retail and eCommerce companies are no longer competing solely on price, assortment, logistics, or brand. As AI systems increasingly mediate how products are discovered, compared, explained, and recommended, retailers are now competing on a new axis:

How clearly their commercial authority, category relevance, and trust signals can be interpreted — or deliberately withheld — by machines.

In this environment, AI is not just a shopping assistant. It is an intermediary. It decides which retailers are surfaced as authoritative, which product narratives are reused, and which brands become default answers to consumer intent.

This shift introduces a new strategic layer for retail — one that sits above merchandising and below logistics — where visibility, legibility, and access posture quietly determine influence over demand.

This report examines how major global eCommerce and retail organizations are positioning themselves within that layer.

The Structural Shift: From Distribution to Discovery

Historically, retail advantage was driven by physical footprint, supplier leverage, pricing power, and fulfillment efficiency. Those factors still matter. But AI introduces a parallel economy of discovery — one where:

- Products are summarized before being browsed

- Brands are compared before being considered

- Retailers are interpreted before being chosen

As a result, retailers are no longer just competing for shelf space or search rankings. They are competing to shape machine trust at the moment of intent.

Unlike media or finance, retail exhibits wide dispersion. Many firms remain open by default, but few have engineered strong entity clarity. Others deliberately block AI access to protect brand or membership economics — often without realizing the long-term discovery tradeoff.

The result is a fragmented chessboard where scale, brand, and AI legibility are misaligned.

The Emerging eCommerce Chessboard

The retail landscape in the AI era shows a three-layer structure.

At the top are retailers that combine openness with exceptional structural clarity. These organizations — such as Kroger, Burlington Stores, Ross Stores, and H&M — allow AI systems to understand not just what they sell, but what they stand for. They become trusted category references.

At the bottom are brands and platforms that intentionally or unintentionally remove themselves from AI mediation. Membership retailers, brand-experience companies, and some regional platforms block or severely restrict access, prioritizing control over discovery.

Between these extremes sits the largest group: retailers that are open, crawled, and massive — yet structurally thin. They are visible everywhere, but authoritative nowhere. In an AI-mediated commerce environment, this middle position is the most precarious.

Strategic Archetypes in eCommerce & Retail

Across the dataset, five strategic archetypes emerge. Each reflects a distinct bet on how value will be created and captured as AI becomes a primary interface for shopping, comparison, and intent resolution.

1. Retail Sovereigns

Retail Sovereigns pursue an influence-first strategy. They are open, structurally consistent, and highly legible to AI systems. Grocery, discount, and category-specialist leaders dominate this group.

Kroger stands as the highest-ECC retailer in the entire dataset, followed closely by Burlington Stores, Ross Stores, H&M Group, and Falabella.

These retailers benefit from:

- Clear category ownership

- Consistent product and brand taxonomies

- Strong store-to-entity coherence

AI systems rely on them not just for products, but for context — pricing norms, category comparisons, and value framing.

The tradeoff mirrors finance Market Shapers: insight is given away. But these retailers are betting that being the default reference at intent time compounds more value than controlling every interaction.

2. Defensive Merchants

Defensive Merchants balance visibility with protection. Large incumbents such as Walmart, Home Depot, Target, Dollar General, and Ulta Beauty exemplify this posture.

They maintain strong structural clarity and institutional signals while limiting exposure where margin protection, private labels, or operational complexity demand it.

This posture preserves flexibility:

- Strong AI presence without full commoditization

- Optionality for private AI integrations

- Reduced risk of uncontrolled product abstraction

The downside is slower authority compounding compared to fully open peers.

3. Scale Without Clarity

This is the most crowded archetype — and the most dangerous.

Platforms such as Amazon, Alibaba, JD.com, MercadoLibre, and PDD Holdings operate at enormous scale, yet exhibit surprisingly low AI-level authority. Their size overwhelms structure. Their sprawl dilutes trust.

AI systems can crawl them, but struggle to interpret them as coherent entities. As a result, these platforms are frequently used, but rarely trusted as explanatory sources.

This group faces a paradox: they dominate commerce, yet risk losing narrative control over how commerce is explained.

4. Brand Fortresses

Brand Fortresses deliberately block AI access to protect experience, exclusivity, or membership economics. Costco, Lululemon, Coupang, Tractor Supply, and eBay represent this archetype.

Their strategy is control, not influence. They prioritize:

- Brand experience integrity

- Member-only economics

- Reduced price comparison leakage

Unlike media, blocking does not erase these brands. But it does remove them from AI-driven discovery loops — particularly for new or casual consumers.

This archetype is sustainable for brands with strong loyalty. It is far riskier for those without it.

5. Commodity Retail Pipes

Commodity Retail Pipes are open but structurally undifferentiated. Many regional grocers, department stores, and big-box operators fall here.

AI systems can read them, but rarely cite them. Over time, they risk becoming interchangeable infrastructure — useful for fulfillment, but invisible in recommendation and explanation layers.

Without investment in entity clarity, this group faces quiet commoditization.

What the Data Reveals

Several patterns emerge consistently across the dataset:

- Highest ECC does not correlate with market cap.

- Discount and grocery outperform luxury and platforms in AI clarity.

- Blocking preserves brand control, but forfeits discovery.

- Scale without structure is a liability, not an advantage.

- Retail differs sharply from finance: openness without clarity is punished faster.

Most importantly, the most dangerous position is not being blocked — it is being open, massive, and structurally incoherent.

Strategic Implications for Retail Leadership

The defining question for retail executives is no longer:

“How efficiently do we sell?”

It is increasingly:

“What role do we want to play in the AI-mediated discovery layer?”

Each archetype represents a strategic bet:

- Retail Sovereigns bet on being the default answer

- Defensive Merchants bet on controlled relevance

- Scale Platforms bet on inevitability

- Brand Fortresses bet on loyalty over discovery

- Commodity Pipes bet on volume without authority

AI will not eliminate retail competition — but it will reorder influence.

Retailers that engineer clarity early will shape how products are discovered and compared. Those that do not will continue selling — but increasingly on terms defined by others.

Entity Engineering Standards Lab