Entity Clarity Report — Finance Landscape in the AI Era

Summary

This Entity Clarity Report analyzes how major financial institutions — including global banks, asset managers, exchanges, insurers, and financial infrastructure providers — are positioning themselves in the AI era, where machine interpretation increasingly influences trust, capital flows, and economic narratives.

By examining structural clarity, access posture, and strategic intent, the report maps the emerging financial chessboard and highlights which institutions are shaping AI’s understanding of markets, which are preserving leverage through controlled access, and which risk being interpreted primarily through secondary sources as AI becomes a dominant interface for financial knowledge and decision-making.

Methodology

This report is based on a proprietary Entity Clarity analysis of leading global financial institutions by market capitalization, spanning banking, asset management, insurance, payments, exchanges, and financial data providers.

Institutions analyzed include global systemically important banks, alternative asset managers, financial infrastructure firms, and regional leaders across the United States, Europe, Asia, and emerging markets.

Each organization was evaluated using a 13-signal framework measuring how clearly its identity, authority, and economic role can be interpreted by AI systems. Signals span entity comprehension, structural data fidelity, and page-level hygiene, producing an overall Entity Clarity & Capability (ECC) score.

Importantly, this methodology does not assess financial performance, balance sheet strength, or management quality. Instead, it measures machine-level legibility — how effectively AI systems can discover, understand, and rely on each institution as a source of financial truth.

Strategic posture (Open, Defensive, or Blocked) was assessed in parallel to understand how intent and structure interact in an AI-mediated financial ecosystem.

Run an Entity Clarity Review on any company or brand

Findings

Several findings stand out across the financial dataset:

First, narrative authority compounds faster than balance-sheet scale.

Asset managers such as Blackstone (ECC 91) and BlackRock (ECC 86) rank among the highest Entity Clarity scores in the entire dataset, despite not being the largest institutions by assets. Their openness, structural rigor, and publication depth allow AI systems to rely on them as default interpreters of market dynamics.

Second, decisiveness outperforms ambiguity.

The dataset shows a sharp bifurcation. Institutions that commit fully to openness (e.g., Wells Fargo – ECC 81, Citigroup – ECC 88) or fully to exclusion (e.g., Goldman Sachs – ECC 0, S&P Global – ECC 0, CME Group – ECC 0) exhibit far clearer strategic alignment than those lingering in partial states.

Third, legacy reputation does not translate cleanly to machine authority.

Berkshire Hathaway (ECC 38) stands out as the most extreme outlier in the dataset: the largest company by market capitalization, yet among the weakest in machine legibility. Similarly, JPMorgan Chase (ECC 58) lags structurally behind peers like Citigroup and Wells Fargo, despite its dominance in global banking.

Fourth, exclusion in Finance preserves power rather than eroding it.

Unlike Media, where blocking risks disappearance, financial infrastructure firms such as S&P Global, CME Group, and Mastercard maintain leverage precisely because their data is scarce, proprietary, and monetized directly. Their invisibility to public AI systems does not weaken their economic position.

Finally, several systemically important institutions risk being narratively outsourced.

Large regional and global banks — including Royal Bank of Canada (ECC 5), Charles Schwab (ECC 6), and Scotiabank (ECC 41) — remain open but structurally thin, increasing the likelihood that AI systems describe their markets using third-party sources rather than their own institutional voice.

Landscape

The financial landscape is undergoing a structural reordering as AI systems increasingly summarize markets, contextualize risk, and answer questions on behalf of investors, regulators, and consumers.

Our analysis reveals a barbell-shaped ecosystem:

- On one end, high-clarity, open institutions such as Blackstone, BlackRock, Wells Fargo, Citigroup, and National Australia Bank (ECC 81) actively shape AI-mediated economic narratives.

- On the other end, fully excluded data fortresses — including Goldman Sachs, Morgan Stanley, S&P Global, CME Group, and HDFC Bank — protect proprietary advantage by denying public machine access altogether.

- In the middle sit legacy and regional institutions with uneven optimization, including Berkshire Hathaway, JPMorgan Chase, UBS, Royal Bank of Canada, and Charles Schwab, whose influence increasingly depends on how others describe them.

This polarization reflects intentional strategy, not technical maturity.

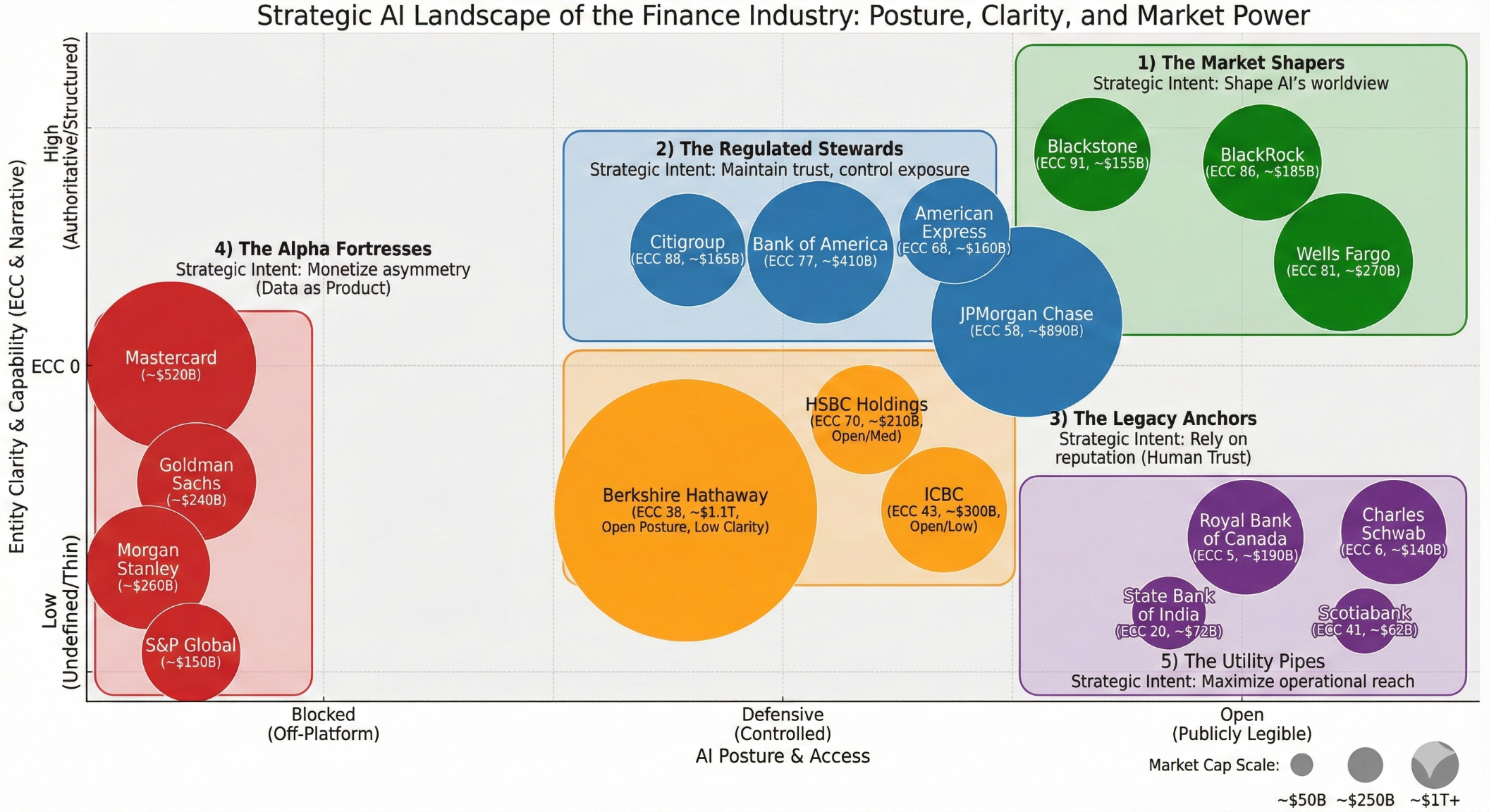

Archetypes

1) The Market Shapers

Posture: Open, structurally strong, narrative-forward

Strategic intent: Shape AI’s economic worldview

Institutions such as Blackstone (91) and BlackRock (86) pursue an influence-first strategy. Their research, outlooks, and frameworks are designed to be legible, reusable, and authoritative to machines.

Strengths

- Disproportionate presence in AI-generated market explanations

- Compounding narrative authority

- Early positioning as reference truth for entire asset classes

Risks

- Giving away strategic insight to competitors

- Monetization lag relative to influence

Trajectory: Most will double down. This strategy already works.

2) The Regulated Stewards

Posture: Defensive access with high structural clarity

Strategic intent: Maintain trust while controlling exposure

Institutions like Citigroup (88), Bank of America (77), and American Express (68) balance AI legibility with regulatory, privacy, and enterprise constraints.

Strengths

- Strong institutional trust signals

- Optionality for private AI partnerships

- Lower risk of narrative misinterpretation

Risks

- Slower influence compounding than open peers

- Dependence on negotiated AI distribution

Trajectory: Likely to cautiously expand controlled exposure.

3) The Legacy Anchors

Posture: High human trust, weak-to-moderate machine grounding

Strategic intent (implicit): Rely on reputation

Berkshire Hathaway (38) is the clearest example. Its structural minimalism forces AI systems to rely on secondary descriptions of a famously complex entity. JPMorgan Chase (58), while stronger, still trails structurally behind Citi and Wells Fargo.

Strengths

- Deep institutional credibility

- Strong resilience in traditional markets

Risks

- Being narratively defined by others

- Gradual erosion of machine-level authority

Trajectory: This group has the highest upside — if leadership acts.

4) The Alpha Fortresses

Posture: Fully blocked

Strategic intent: Monetize asymmetry

Institutions including Goldman Sachs, Morgan Stanley, S&P Global, CME Group, and Mastercard treat data as product, not marketing.

Strengths

- Maximum control over proprietary information

- Strong pricing power in private markets

- Independence from public AI narratives

Risks

- Zero public AI presence

- Long-term dependence on closed ecosystems

Trajectory: Will remain closed; value capture occurs off-platform.

5) The Utility Pipes

Posture: Open but structurally thin

Strategic intent: Maximize operational reach

Institutions such as Royal Bank of Canada (5), Charles Schwab (6), Scotiabank (41), and State Bank of India (20) remain visible but narratively weak.

Strengths

- High transactional relevance

- Broad customer bases

Risks

- Becoming interchangeable infrastructure

- Losing advisory and narrative authority

Trajectory: Stable in the short term, fragile long term.

Index

Strategic Implications

For financial executives, the implications are clear:

- AI systems increasingly decide whose interpretation of markets matters.

- Institutions either shape belief, sell truth, or cede narrative control.

- The most dangerous position is not being blocked — it is being open but unreadable.

- Early clarity advantages compound quietly and unevenly.

The strategic question is no longer whether AI will mediate financial understanding — but who gets to define reality when it does.

Full Report

Executive Framing

Financial institutions are no longer competing solely on balance sheets, pricing, or distribution. As AI systems increasingly mediate how markets are explained, risks are contextualized, and capital is allocated, institutions are now competing on a new axis:

How clearly their authority, worldview, and truth claims can be interpreted — or controlled — by machines.

In this environment, AI is not just a tool. It is an intermediary. It decides which institutions are cited, which frameworks are reused, and which narratives become default explanations of economic reality. This shift creates a new strategic layer for finance — one that sits above products and below regulation — where visibility, legibility, and access posture quietly determine influence.

This report examines how major global financial institutions are positioning themselves within that layer.

The Structural Shift: From Products to Perception

Historically, financial advantage was driven by scale, access to capital, proprietary information, and regulatory positioning. Those factors still matter. But AI introduces a parallel economy of perception — one where:

- Market explanations are summarized before being read

- Risk is contextualized before being priced

- Institutions are interpreted before being chosen

As a result, financial institutions are no longer just competing for customers or counterparties. They are competing to shape machine trust.

Our analysis reveals that finance, unlike media, has largely avoided indecision. Institutions tend to make clear, deliberate bets about their role in the AI ecosystem. They either aim to influence the narrative openly, or they aim to protect proprietary truth behind controlled or blocked access. Very few attempt to sit in the middle.

The Emerging Finance Chessboard

The financial landscape in the AI era exhibits a barbell structure.

On one end are institutions that deliberately maximize openness and clarity. These organizations — most notably large asset managers and capital allocators — want AI systems to understand their views of markets, risk, and opportunity. Their strategy is influence-first: if AI becomes the default interpreter of economic reality, they want their frameworks embedded in that interpretation.

On the opposite end are institutions whose data is the product. Market data providers, exchanges, payment networks, and investment banks derive value from exclusivity and asymmetry. For them, public AI visibility is not an asset — it is a liability. These firms deliberately block or restrict access, preserving leverage by ensuring that truth must be purchased, not inferred.

Between these poles sit legacy and regulated institutions whose human authority remains enormous, but whose machine-level clarity is uneven. In an AI-mediated world, this middle position carries the greatest strategic risk: being open enough to be read, but not clear enough to be trusted.

Strategic Archetypes in Finance

Across the dataset, five strategic archetypes emerge. Each represents a distinct bet on how value will be created and captured as AI becomes a primary interface for financial understanding.

1. Market Shapers

Market Shapers pursue an influence-first strategy. These institutions are open, highly structured, and intentionally legible to machines. Asset managers such as Blackstone and BlackRock exemplify this posture.

Their research, outlooks, and thematic narratives are designed to be reusable by AI systems. The objective is not short-term attribution, but long-term authority: becoming the default reference point for how markets, asset classes, and macro trends are explained.

This strategy compounds quietly. As AI systems repeatedly rely on these institutions for context, their worldview becomes normalized — and influence grows without explicit distribution.

The tradeoff is obvious: insight is given away freely. But these institutions are betting that authority attracts assets, and assets dwarf content value.

2. Regulated Stewards

Regulated Stewards balance openness with control. Large banks and consumer-facing financial institutions such as Citigroup, Bank of America, and American Express fall into this category.

They maintain strong structural clarity and institutional signals, while restricting access where regulatory, privacy, or enterprise considerations require it. Their goal is not mass influence, but trusted presence — remaining legible and credible to AI systems without exposing sensitive or proprietary material.

This posture preserves optionality. It allows for private AI partnerships, enterprise tools, and negotiated distribution, while avoiding reputational risk from uncontrolled interpretation.

The downside is slower influence compounding relative to fully open peers.

3. Legacy Anchors

Legacy Anchors are institutions whose human reputation far exceeds their machine-level clarity. Berkshire Hathaway is the most striking example: the largest company in the dataset by market capitalization, yet one of the weakest in AI legibility.

These institutions rely on brand gravity, historical credibility, and institutional trust to sustain relevance. In the short term, this works. In the long term, it creates a dependency on secondary interpretation — analysts, media, and third-party summaries increasingly define how AI systems understand them.

This group carries the greatest upside and the greatest risk. With relatively modest structural investment, many could leap into influence. Without it, they risk ceding narrative control while remaining economically dominant.

4. Alpha Fortresses

Alpha Fortresses treat information as inventory. Investment banks, exchanges, market data providers, and payment networks — including Goldman Sachs, S&P Global, CME Group, and Mastercard — deliberately block public AI access.

Their strategy is not visibility, but monetization. They sell verified truth, not opinion. In this model, AI systems are customers, not audiences.

Unlike media companies that risk fading from relevance when blocked, financial Alpha Fortresses remain structurally indispensable. Their exclusion does not weaken them; it preserves pricing power and asymmetry.

This archetype is likely to remain stable. These institutions will participate in AI through private channels, exclusive licensing, and proprietary tools — not open crawls.

5. Utility Pipes

Utility Pipes are open, widely accessible institutions with low structural differentiation. Regional banks, brokers, and transactional platforms such as Royal Bank of Canada, Charles Schwab, and Scotiabank exemplify this posture.

They are operationally critical but narratively weak. AI systems can read them, but rarely rely on them as sources of authority. Over time, this risks relegating these institutions to infrastructure — used, but not trusted for interpretation or advice.

Without investment in entity clarity and narrative framing, this group faces gradual commoditization.

What the Data Reveals

Several patterns are consistent across the dataset:

- Decisiveness matters more than intent. Institutions that fully commit — either to openness or exclusion — outperform those that drift.

- Narrative power compounds silently. High-ECC institutions shape AI outputs without explicit attribution.

- Reputation does not translate automatically. Machine trust must be engineered.

- Finance differs fundamentally from Media. Blocking in finance preserves leverage; blocking in media risks disappearance.

Most importantly, the most dangerous position is not being blocked — it is being open but unreadable.

Strategic Implications for Financial Leadership

The defining strategic question for financial institutions is no longer:

“How strong is our balance sheet?”

It is increasingly:

“What role do we want our institution to play in the AI truth ecosystem?”

Each archetype reflects a conscious bet:

- Market Shapers bet on influence becoming capital

- Regulated Stewards bet on trust under governance

- Legacy Anchors bet on reputation buying time

- Alpha Fortresses bet on scarcity and control

- Utility Pipes bet on scale without authority

AI will not flatten finance — but it will reorder influence.

Institutions that understand this early will shape how markets are explained. Those that ignore it will still operate — but increasingly on terms set by others.

For Further Reading:

Entity Engineering Standards Lab

Entity Clarity Report - Media Landscape

Entity Clarity Report - eCommerce & Retail Sector