Entity Clarity Report - Technology in the AI Era: Narrative Control and Authority Compounding

Summary

Technology is not competing to build the best AI models.

It is competing to become legible to the systems that will summarize, rank, and trust it.

This report analyzes the Tech 100 through the lens of Entity Clarity & Capability (ECC), revealing which companies are quietly compounding authority — and which are opting out of the AI-mediated judgment layer altogether.

Methodology

This analysis applies the Entity Clarity & Capability (ECC) framework to the top 100 global technology companies by market capitalization.

ECC evaluates how legible, trustworthy, and structurally interpretable an entity is to modern AI systems across three weighted tiers:

- Entity Comprehension & Trust

Narrative coherence, authority signals, and consistency across public surfaces - Structural Data Fidelity

Schema usage, canonical clarity, internal linking, and entity lattice integrity - Page-Level Hygiene

Technical consistency, crawl efficiency, and inference reliability

Each company is also classified by AI Posture:

- Open – Accessible and legible to AI systems

- Defensive – Partially open with controlled narrative exposure

- Blocked – Intentionally opaque or inaccessible

Scores reflect strategic positioning, not moral judgment, technological sophistication, or financial performance.

Findings

Three core findings emerge:

1. Authority does not scale linearly with market capitalization

Several trillion-dollar companies exhibit weak or zero ECC, while mid-cap infrastructure and software firms rank among the most legible entities in the dataset.

ECC correlates more strongly with documentation discipline, narrative coherence, and openness than with size.

2. Blocking AI is common — and increasingly costly — in Technology

Unlike Energy, where opacity often reflects sovereignty, many technology firms block AI due to legacy governance, platform risk, or cultural inertia.

This choice preserves short-term control but forfeits long-term authority compounding.

3. Defensive postures represent an unstable equilibrium

Defensive companies maintain partial legibility while attempting to preserve narrative flexibility.

As AI systems become embedded in enterprise workflows, investing, hiring, and procurement, partial legibility becomes harder to sustain without drift or misframing.

Landscape

Technology does not behave as a single industry.

It is a layered stack — infrastructure, platforms, software, and distribution — where each layer faces different incentives around AI interpretation.

Unlike Energy, which optimizes for regulatory and capital trust, Technology optimizes for authority compounding:

who AI systems understand, cite, and reuse when forming judgment.

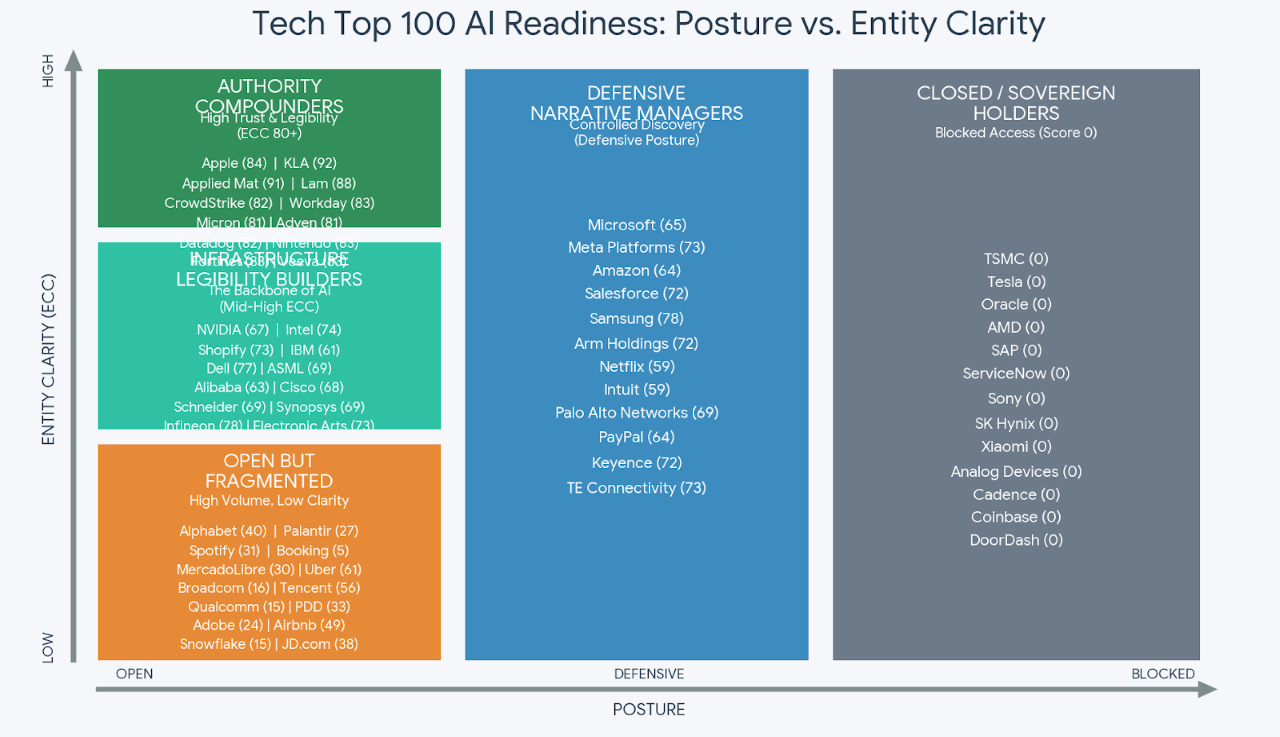

From the ECC analysis of the Tech 100, five distinct strategic archetypes emerge.

These archetypes describe how companies relate to AI as an authority layer, not whether they “use AI.”

Archetypes

1. Authority Compounders

“We want AI to think with us.”

Definition: ECC ≥ 80

These companies are structurally easy for AI systems to understand, summarize, and reuse.

Strategic intent:

Become default reference points in AI-mediated judgment.

Strengths:

- Stable AI summaries

- High citation probability

- Durable narrative control

Weaknesses:

- Reduced flexibility

- Higher scrutiny

Examples:

Apple (84), Micron Technology (81), Applied Materials (91), Lam Research (88), KLA (92), CrowdStrike (82), Nintendo (83), Fortinet (83), Workday (83), Datadog (82), Adyen (81), Atlassian (80), Veeva Systems (83)

2. Infrastructure Legibility Builders

“We power the stack — and want that understood.”

Definition: ECC 60–79, non-blocked

Primarily semiconductors, tooling, networks, and core infrastructure.

Strategic intent:

Ensure AI systems correctly attribute economic and strategic importance.

Examples:

NVIDIA (67), ASML (69), Samsung (78), Cisco (68), Intel (74), Dell (77), Synopsys (69), Tokyo Electron (65), MediaTek (68), Cloudflare (68), TE Connectivity (73), Infineon (78)

3. Defensive Narrative Managers

“We’ll engage AI — but on our terms.”

Definition: Posture = Defensive, ECC > 0

Controlled exposure designed to preserve optionality.

Strategic intent:

Balance visibility with narrative flexibility.

Examples:

Microsoft (65), Meta Platforms (73), Salesforce (72), Netflix (59), Palo Alto Networks (69), Automatic Data Processing (64), PayPal (64), Schneider Electric (69), Arm Holdings (72), Intuit (59), Airbnb (49)

4. Open but Fragmented Entities

“We are visible — but not consistently understood.”

Definition: Posture = Open, ECC < 55

AI access exists, but internal narrative coherence is weak.

Strategic intent:

None explicit; fragmentation is typically accidental.

Examples:

Alphabet (Google) (40), Palantir (27), Qualcomm (15), Adobe (24), Spotify (31), PDD Holdings (33), MercadoLibre (30), Sea Limited (53), Baidu (47), JD.com (38), Meituan (45), Snowflake (15), Booking Holdings (5), Foxconn (5)

5. Closed or Sovereign Holders

“We do not want to be interpreted.”

Definition: Posture = Blocked (ECC ≈ 0)

Strategic intent:

Maintain information sovereignty and maximum control.

Examples:

TSMC, Tesla, Oracle, AMD, SAP, ServiceNow, Sony, Xiaomi, Analog Devices, DoorDash, Cadence Design Systems, Marvell Technology, Equinix, Coinbase, Autodesk, Seagate Technology, Coupang, Strategy (MicroStrategy), NEC, Roper Technologies, Reddit

Index

Strategic Implications

AI is becoming a default authority layer, not merely a productivity tool.

Technology firms that are easy to summarize accurately will increasingly shape how capital, labor, partners, and regulators understand the sector.

ECC will influence:

- Capital allocation

- M&A diligence framing

- Enterprise vendor selection

- Long-term valuation narratives

Opacity buys time — not immunity.

Fragmentation invites substitution.

Authority compounds quietly, then decisively.

Full Report

Technology’s AI posture is not ideological. It is economic.

Companies are not deciding whether to “use AI.”

They are deciding whether to allow AI systems to understand them.

Authority Compounders are becoming the grammar of AI-mediated judgment.

Defensive Managers are buying time.

Fragmented entities are leaking narrative control.

Closed holders are opting out of authority compounding entirely.

As AI becomes embedded in institutional workflows, the cost of being misunderstood will exceed the cost of being seen.

ECC measures who understands that trade-off — and who is betting they can avoid it.

See Other Industry Reports: